Investing your third pillar assets: options, risks, and returns

27 April 2026 | Comment(s) |

Lesly Kiameso

The third pillar is a retirement planning tool that is designed to adapt to the major stages of your life. Buying a home, starting a business, moving abroad, protecting your family, or simply preparing for a comfortable retirement: many of these projects begin with a well-structured retirement strategy.

However, between tax considerations, investments, and asset allocation, it’s perfectly normal to feel overwhelmed. In this article, we explain what people don’t always take the time to explain in depth when it comes to investing your third pillar, particularly the pillar 3a.

Tax savings: the primary “return” under the third pillar

Before discussing financial performance, it is essential to understand why tax savings represent the most tangible benefit of pillar 3a. Unlike the return on a fund or financial market, the tax benefit is guaranteed, immediate, and completely independent of economic fluctuations.

Contribution strategies and calculation of the tax impact

Here is a concrete example for a 30-year-old taxpayer, single and residing in Lausanne:

- Gross annual income: CHF 100,000

- Marginal tax rate: 31.7%

- Annual contribution under pillar 3a: CHF 7,258

- Estimated tax upon withdrawal: CHF 17,740

Summary :

| Items | Amounts (CHF) |

|---|---|

| Annual contribution | 7,258 |

| Duration (years) | 35 |

| Total invested | 254,030 |

| Annual tax savings | 2,291 |

| Total tax saving | 80,185 |

| Tax upon withdrawal | 17,740 |

| Net profit after tax | 316,575 |

Tax savings therefore represent a significant financial lever, one that is often underestimated. It is the primary component of the overall return on a pillar 3a account.

How is a withdrawal under the pillar 3a taxed?

Withdrawals from a pillar 3a account are taxed separately from other income, at a reduced and progressive rate. The exact amount depends on your canton of residence, but tax treatment is generally much more favourable than standard income tax. The higher the amount withdrawn, the higher the tax rate, which sometimes makes it advisable to stagger pillar 3a withdrawals whenever possible.

Inflation: a silent enemy of your purchasing power

Inflation, otherwise known as the general rise in prices over time, gradually erodes the real value of your savings, even when it seems low. For example, if you leave CHF 7,258 (the maximum 3a amount) in an account with a return that is lower than inflation, then:

- After 10 years, that amount of CHF 7,258 has a purchasing power equivalent to only about CHF 5,940.

- After 20 years, its real purchasing power is close to CHF 4,860.

- After 35 years, it is worth only about CHF 3,600.

The tax savings from a pillar 3a account far exceed inflation. In our example, saving CHF 2,291 per year already equates to a return of 31.57%, well above an inflation rate of 2%. But this is an immediate benefit. To grow your capital over time, investing then becomes the most relevant strategy.

Investment options for your third pillar

How can you make this capital grow in nominal terms over several years? Over the long term, the goal is not only to protect the real value of the money but to increase the capital amount in nominal terms. Historically, markets, and global equities in particular, are among the investment vehicles that have generated significant nominal growth over several decades.

Therefore:

- The tax advantage is the foundation (immediate return).

- Investment builds everything else (return over time).

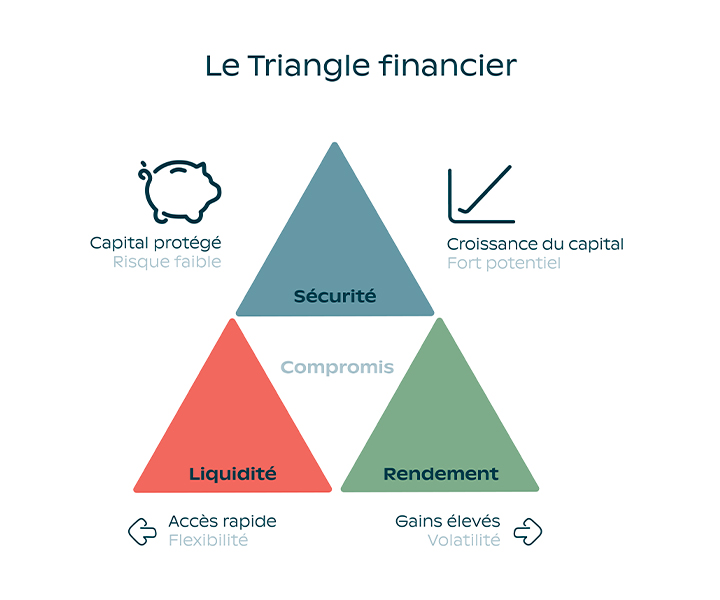

The financial triangle: pillar 3a checks all the right boxes

First and foremost, it is essential to understand how the financial triangle works. Every investment involves a trade-off between three objectives: security, liquidity, and return.

In investment terms, an investment is a trade-off between these three factors. Pillar 3a offers less liquidity (funds are locked in until retirement, with exceptions for early withdrawals) to provide a secure framework and potential for long-term returns. This is precisely what creates the tax advantage.

Savings, investments, or hybrid strategies?

- If you opt for a 3a savings account, you prioritize security with guaranteed capital, for a limited return (often below inflation).

- If your strategy is focused on “investments,” such as investment funds, you are betting on long-term growth while accepting limited liquidity and market fluctuations.

- A hybrid strategy combines secure savings with dynamic investments, allowing you to benefit from a higher return while limiting sharp fluctuations.

Life insurance and the third pillar

A third pillar in the form of life insurance includes coverage in the event of death and/or disability. It thus offers additional security but involves often higher fees that delay profitability. This solution is particularly well-suited for people seeking to combine savings and protection over the long term. In some cases, combining insurance with a 3a bank account can be a wise option.

The time horizon: the most powerful lever

When starting to invest, people often think that the markets are “too risky.” In reality, time is your best ally because the longer the time horizon, the more crises (such as those in 2008 or 2020) become mere episodes in an overall positive trajectory. Investing remains a highly attractive option.

A third pillar typically involves a 25- to 40-year time horizon. Over this period, major stock market indices like the MSCI World have posted an average return of 8–10% per year over several decades. For your investment, this means that:

- Crises are normal.

- They never last as long as your retirement horizon.

- The time horizon absorbs shocks and maximizes the chances of a positive outcome.

What are the goals behind a third pillar account?

The “time” factor must be taken into account from the very start when setting up a third-pillar solution. Planning for retirement requires a stable long-term strategy, whereas buying real estate requires savings to be available sooner. If you’re planning to pass assets on to the next generation, it’s best to prioritize solutions that offer protection for your loved ones.

Adapting your strategy over time

Your age and investment horizon directly influence your investment strategy. The younger a person is, the larger the portion they can allocate to stocks, as time will more easily absorb market fluctuations. As retirement approaches, it is often advisable to reduce risk and gradually secure your capital.

Strategic asset allocation: the driver of performance

Asset allocation refers to how your money is distributed across different types of investments: stocks, bonds, real estate, cash, etc. The “allocation strategy” is the primary driver of long-term performance.

Why? Because each asset class reacts differently depending on the economic context:

- Stocks rise over long periods and reward risk in the long term. They have been the best-performing asset for over 100 years, according to the Global Investment Returns Yearbook 2025. In particular, stocks in the MSCI World Index generated an annualized return of 8% to 10% per year between 1978 and 2025.

- Bonds play a stabilizing role.

- Cash provides security… but a low return.

- Real estate offers additional diversification.

How can you grow your third pillar?

Since pillar 3a is a very long-term investment (20 to 40 years), the main objective is not to avoid short-term market fluctuations, but to accumulate maximum nominal growth. This is achieved through stocks, particularly global ones, which involve short-term volatility but subsequently guarantee better return potential. This is why banks and insurance companies offer 80–100% stock strategies designed for very long-term horizons, such as retirement.

A good asset allocation depends on three simple parameters:

- Your time horizon: the longer it is, the more you can use equities to drive growth.

- Your risk tolerance: if market fluctuations stress you out, you can include more bonds to smooth out volatility.

- Your objective: for a pillar 3a, the objective is clear: capital growth for retirement. The allocation should therefore be geared toward performance, not toward maximum safety (which erodes value over 30 years).

VariaInvest: Groupe Mutuel’s third pillar solution

Combine security, flexibility, and return potential with VariaInvest, a 3a or 3b pension solution that adapts to your goals, protects your loved ones, and offers real growth potential.

Discover VariaInvestChoose your investor profile

With VariaInvest, you can combine security and performance in the proportions that suit you and adjust your strategy as your life changes, choosing from five investment plans:

- 100% guaranteed (Security)

- 75% guaranteed / 25% funds (Conservative)

- 40% guaranteed / 60% funds (Balanced)

- 100% funds (Dynamic)

- 100% equity-oriented funds (High-Growth)

A flexible and high-performing solution

Career, family, plans, or unexpected events: VariaInvest adapts to your life journey. Choose a more conservative plan when you’re consolidating and a more dynamic one when the outlook brightens. And because flexibility is a useful luxury, make additional contributions, choose portfolio rebalancing options, and activate the protection of invested savings (to safeguard gains when markets rise).

VariaInvest can be combined with highly strategic risk coverage:

Death: to protect your loved ones and your plans

Disability: to safeguard your ability to save and your income

Premium waiver: your plan continues even in the event of a setback

Lump-sum payment in case of hospitalization/birth: a targeted reserve for key moments

Together with your advisor, you define an investor profile and a plan perfectly tailored to your risk tolerance, your goals, and your financial situation. Get free, no-obligation retirement planning advice from our experts!

Investing in your third pillar: what you need to know

- What is the tax advantage of the third pillar?

The tax advantage is the first return: every 3a contribution immediately reduces your taxes and boosts your savings.

- How does inflation affect my third pillar?

Inflation erodes uninvested savings. Investing is therefore essential to preserve and grow the real value of your capital.

- What role does time play in third pillar investing?

Time reduces risk. Over 20–40 years, markets have always rebounded and generated returns despite crises.

- What optimizes the return on my third pillar?

Stocks are the engine of long-term growth. They offer the best returns over several decades, making them ideal for your retirement savings.

- What is the best strategy for investing my third pillar?

A good asset allocation + a flexible product = sustainable performance. Tailoring your third pillar to your profile, your plans, and the markets maximizes growth potential.